There are many reasons why you might want Chase to increase the credit limit on one of your cards. There is the obvious reason: that you are planning to make large upcoming purchases for yourself or a buying group. Beyond that, a Chase credit line increase may allow you to ramp up your manufactured spending. The Chase Ink cards are some of the best for manufactured spending because of their 5x category bonus on office supply stores. Likewise, the Chase Freedom’s rotating 5x category bonuses make it easy to rack up an additional 30,000 Ultimate Rewards points each year.

You can request a Chase credit line increase online or by calling Chase. This will trigger a hard inquiry on your credit report. Alternatively, if you update the annual income listed in your Chase profile, Chase may grant you an increase at some point without a hard pull.

This post will walk you through how to increase your credit limit with Chase, why you might want an increase, and why you might want to transfer credit or apply for a new card instead.

Where to request A Chase credit limit Increase

It’s straightforward to request a credit line increase with Chase. You can do so at chase.com/increasemyline. Alternatively, call Chase at 1-800-432-3117 (personal cards) or 1-888-269-8690 (business cards). You can also use the number listed on the back of your card.

Why you should request a higher limit

Even if you already have a high enough credit line for your purchases or manufactured spending, a greater limit may increase your credit score.

One of the critical factors in your credit score is your credit utilization ratio. In fact, according to Credit Karma, it counts for around 20% of your score. This metric takes the combined balance of all your personal cards and loans as of your last statement dates as a percentage of your total accessible credit. If you were approved for a card several years ago with a low credit limit and you continue to put significant spend on the card, it may make sense to request a higher limit.

A Chase credit line increase request triggers a Hard pull

Any card member-initiated request for a credit line increase with Chase will result in a hard pull on your credit report. Some of the other banks, including Amex and Discover, will approve you for a credit limit increase request without a hard pull. Citi will sometimes require a hard pull, but they will tell you before doing so.

A hard pull will result in a temporary decrease in your credit score, but the impact will diminish within a few weeks.

If you make the request online, you should be warned about a hard pull. However, if you are requesting over the phone, ask if Chase can approve you using only a soft pull.

Chase pulls from one of the three major credit bureaus (Equifax, Experian, or Transunion) but does not consistently pull from the same one. Instead, the bureau varies by the state you reside in and the card you are applying for. Doctor of Credit has a useful post with the bureaus Chase has pulled from for each state.

If you decide to request an increase on multiple cards on the same day, Chase will combine those inquiries and only perform one hard pull. Unfortunately, there are conflicting data points on whether Chase will combine hard pulls if you apply for a new card and request a credit line increase on an existing card the same day.

how to get a Chase credit line increase without a hard pull

There is a way to get a credit line increase with Chase, without a hard pull on your credit report.

From time to time, Chase may reevaluate your credit profile and provide you with an increased credit line without you even asking. While there is no clear way to trigger one of these automated reviews, they often seem to occur after the income listed in your Chase profile is updated.

Sometimes Chase will prompt you to update your income when you log in to your account, but you should really do this whenever your income changes.

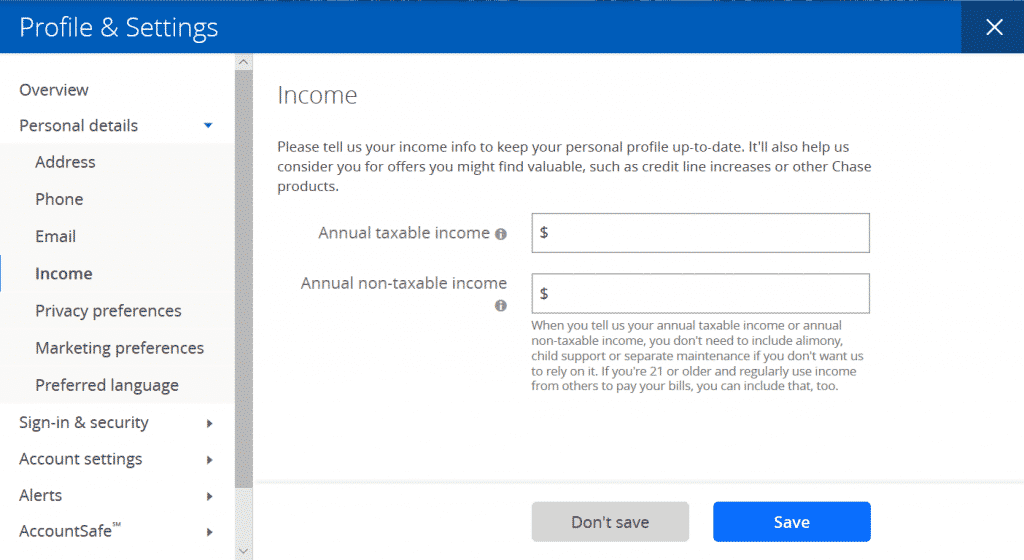

Once you’ve logged into Chase, click the person-looking icon that appears in the top right, and choose “Profile and Settings.” Then, under “Personal Details,” click “Update Info,” and then in the left menu, select “Income.” This should take you to a page that looks like the screenshot below.

When Chase grants you a credit limit increase, they will usually notify you through a secured message or letter in the mail.

Criteria to get a credit line increase

When evaluating your request for a credit line increase, Chase will look at your overall credit profile as well as your spending and payment history on the specific card you are requesting the increase for and any other Chase cards.

You will also need a decent credit score. As mentioned, Chase will either perform a hard or soft pull on your credit report before approving any increase. Therefore, before making the request, you should check your credit score. There is no minimum score required to be approved for a higher limit, but in general, a score below 700 will lower your chances of approval significantly.

You can check your score through a free credit monitoring service like Credit Karma or Credit Sesame, or view your Transunion score through Chase’s Credit Journey.

Chase will then look at your use of their cards. First and foremost, they will want to see that you are paying the statement balance in full or at least a significant portion each month.

Beyond that, Chase wants to see you utilizing a modest proportion of your existing line. On the Credit Journey page, Chase cites “using less than 30% of your credit limit” as having a positive effect on your score. This may sound counterintuitive since the reason you are applying for a higher line is that you are spending close to your current limit. Ideally, though, you should ask for the larger limit before you really need to utilize it.

Chase also does not like to see you cycling through your credit line. Cycling is when you spend a significant portion of your limit, pay it off, and spend it again in the same statement period. Most issuers will classify this as unusual activity, and may even close your account for doing so. As is often the case in the manufactured spending and travel hacking worlds, moderation is key.

They may also look to see if your existing credit line to income ratio is below 50%: Various data points indicate Chase will only extend credit up to 50% of your annual income. If you list $60,000 of annual income on your application but already have $30,000 of credit across your Chase cards, you may be denied. There also seems to be a $65,000 limit on the total amount of credit Chase will extend you across all cards, but this is not explicitly stated anywhere.

Finally, you should wait at least six months after opening the card before requesting an increase. This isn’t a hard rule, but rather a general guideline. Unless your credit profile or income has drastically changed since you applied for the card, you should wait before requesting a higher limit.

Transfer credit from other cards

If you already have sufficient credit on your other Chase cards, it may make sense to re-allocate credit instead of requesting a higher limit. This can be done through a secure message or by calling Chase at the number on the back of your card. I have used the secure message feature to request this several times and have always received a response within a few hours.

You can request to transfer credit between any personal cards or between any business cards. However, you cannot transfer credit from a personal to a business card or a business to a personal card.

Transferring credit will only result in a soft pull. The only exception is if the card you are transferring credit to will end up with more than a $35,000 limit. In that case, Chase may require a hard pull, and you are probably better off just requesting a line increase.

Transferring credit is only a soft pull and will not damage your credit score. However, if you’re requesting a transfer to a card that will end up having a limit higher than $35,000, Chase may require a hard pull.

Moving credit between cards can also be a good idea if you are planning to close a card and could use the credit line on another card.

When to apply for a new card instead

As discussed, any manually requested Chase credit line increases will result in a hard pull on your credit report. Therefore, it may make more sense to apply for a new Chase credit card instead.

If you are under 5/24, meaning you have opened less than five personal credit cards in the past 24 months, you should apply for one of the cards that has a 5/24 restriction.

While requesting a credit line increase on an existing card will not add to your 5/24 count, it may make you less likely to be approved for a new card in the near term.

Many of Chase’s cards, particularly the Visa Signature products, require a minimum credit line of $5,000. Therefore, even if you only had $26,000 of existing credit with Chase and an income of $60,000, you may still be denied.

If you are approved for a new card, you can always transfer credit from your new card to another card as long as you maintain the minimum credit limit on each card.

Bottom Line

Requesting a higher credit line from Chase is a smart way to plan for large purchases or increase capacity on a card that you are using to manufacture spend. If you have a decent credit score, pay off your statement balance in full, and do not have high utilization, you have a good shot at getting approved for a higher limit.

However, any request comes at the price of a hard pull that will temporarily lower your credit score.

You may be able to avoid a hard pull by updating the annual income information in your Chase profile. While not always the case, doing so may result in Chase increasing your limit in due course without you even asking.

Unfortunately, a credit line increase may make it harder for you to get approved for new Chase cards in the future automatically. Chase will only extend so much credit to one customer. Instead of requesting a credit line increase, consider applying for a new Chase card and re-allocating your credit from other cards.